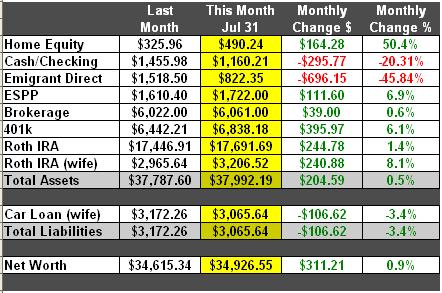

Although I was worried for much of the month that we weren’t going to, we barely managed to pull out a positive month with .9% increase of $311.21. That doesn’t leave a feeling of much acomplishment for the month. We did have some increased expenses which account for some of the lack luster gains including car repairs, a vacation, and 3 family birthdays, including my wife’s. Unfortunately, the extra expenses look to continue in August with tuition due, another vacation, and our anniversary.

Those of you who follow my net worth may have noticed that I decided to start including home equity into my net worth calculation. I wasn’t sure that I wanted to, but decided to in the end. Although we can’t easily tap into that money, part of the reason for buying a home was to start investing our money into an asset rather than throwing it away on rent and a large proportion of our income goes towards paying the mortgage so it should be represented in the net worth calculation. I am using a super conservative method to calculate the amount and it doesn’t take inot account any appreciation.

My wife was excited to see that her asset contribution “Roth IRA (wife)” is now worth more than her liability “car loan (wife)” for the first time. Of course her asset contribution is actually much more when you consider her share of the checking, savings, Emigrant Direct etc.

While I do forsee several expenses this August, I don’t think it can be as bad as last August where our net worth dropped nearly 25% in one month, and I’m grateful for that.

Interesting blog! I was wondering, if you’re going to include your home equity, why you also don’t include your home debt as a liability?

The end result is the same right? I could say I have a home asset of $250,000 and a liability of $249,500. The big numbers would mean the same thing, they’d just make things less readable.